Emirates NBD (DFM: EmiratesNBD), the UAE's largest lender, delivered a solid set of results with net profit up 2% to AED 7.24 billion.

Net profit up 2% to AED 7.24 billion

Proposed dividend maintained at 40%

Dubai, 16 January 2017

Emirates NBD (DFM: EmiratesNBD), the UAE’s largest lender, delivered a solid set of results with net profit up 2% to AED 7.24 billion. The operating performance was helped by further recoveries from legacy impaired loans which offset lower non-interest income. Net interest income declined 1% as a contraction in margins more than offset asset growth. These results have enabled the Board of Directors to recommend to maintain the 2016 dividend at 40 fils per share.

Financial Highlights – FY 2016

- Net profit of AED 7.24 billion, up 2% y-o-y

- Total Income of AED 14.7 billion, declined 3% y-o-y mainly due to lower non-interest income.

- Total assets at AED 448.0 billion, up 10% from end 2015

- Customer loans at AED 290.4 billion, up 7% from end 2015

- Customer deposits at AED 310.8 billion, up 8% from end 2015

- Net Interest Income declined 1% as a contraction in margins more than offset asset growth.

- Core gross fee income held steady despite one-off impact in Q4-16 from the Egyptian Pound devaluation whilst income from property and investments securities declined on lower disposals.

- Cost of risk improved to 83 basis points as impairment charge of AED 2,608 million is 23% lower than in 2015, helped by over AED 3 billion of writebacks and recoveries

- Enhanced asset quality during 2016 as Impaired Loan ratio improved to 6.4% whilst the Impaired Loan Coverage ratio strengthened to 120.1%.

- Advances to Deposit ratio at 93.4% remains comfortably within the management’s target range

- The Bank prudently raised over AED 20 billion of term debt at competitive pricing, through private placements, a sukuk issue and a club loan which further boosted structural liquidity

- Tier 1 Capital Ratio, at a healthy 18.7%, grew on the back of retained profit

- Proposed dividend maintained at 40 fils per share

Commenting on the Group’s performance, His Highness Sheikh Ahmed Bin Saeed Al Maktoum, Chairman, Emirates NBD said: “2016 marked another successful year for Emirates NBD as we continued to deliver improved profitability and a stronger balance sheet amid a challenging environment. We are proud to have launched a number of digital initiatives to support the ‘Smart Dubai’ vision of His Highness Sheikh Mohammed Bin Rashid Al Maktoum, Vice President and Prime Minister of the UAE and Ruler of Dubai. These include a futuristic banking space as part of Dubai Future Foundation’s prestigious Museum of the Future and a pilot blockchain network for international remittance and trade finance. I am very pleased to announce that Emirates NBD has been granted licenses to open 3 additional branches in the Kingdom of Saudi Arabia and our first branch in India. As a leading bank in the region and a front-runner in digital banking innovation, we are well placed to take advantage of growth opportunities within the region. In light of the solid performance by the Bank, we are proposing to maintain the cash dividend at 40 fils per share.”

Mr. Hesham Abdulla Al Qassim, Vice Chairman and Managing Director, Emirates NBD said: “Despite challenging economic conditions, Emirates NBD has delivered a healthy set of financial results. 2016 marked a year of digital innovation as the Bank made bold strides in advancing our digital banking capabilities and the multichannel transformation of our processes, products and services. We are very pleased to have been awarded, for the second consecutive year, ‘Bank of the Year’ in the UAE by The Banker. This recognises Emirates NBD’s strong financial profile and pioneering approach to the digitalisation of banking. The Group is well positioned to utilise our strong franchise, capital and liquidity base to take advantage of growth opportunities in our preferred markets. We are confident that, going forward, our prudent business model shall continue to deliver a solid performance and deal with the opportunities and challenges that will present themselves.”

Group Chief Executive Officer, Shayne Nelson said: “Emirates NBD delivered a solid performance in 2016. Net profit increased by 2% to AED 7.24 billion, underpinned by asset growth, a control on expenses and an improved cost of risk. The Bank’s stable and resilient financial profile were recognized by Moody’s in June when they upgraded Emirates NBD’s long-term rating to A3. The Group’s liquidity position remained strong, bolstered by a stable and highly diversified deposit base and our ability to raise over AED 20 billion of term funding. Given the ongoing challenging environment, we will remain focused on controlling expenses and managing risks whilst ensuring that we continue to invest to support future growth. I am confident that Emirates NBD will continue to deliver excellent customer service and superior value to our shareholders.”

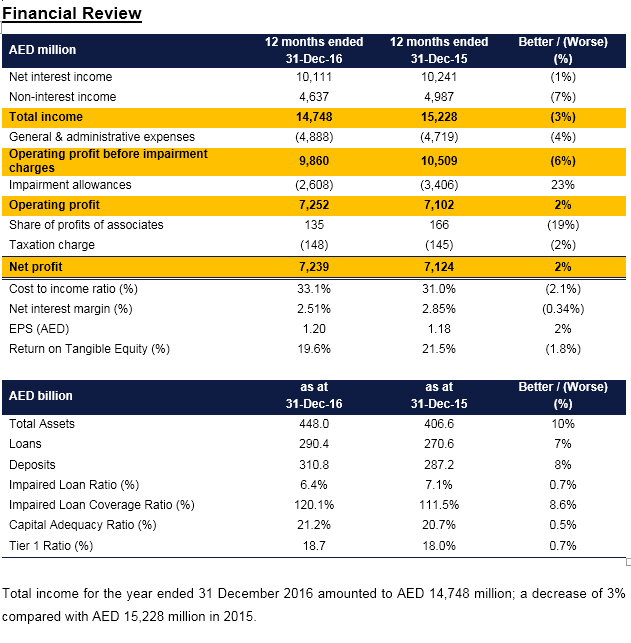

Total income for the year ended 31 December 2016 amounted to AED 14,748 million; a decrease of 3% compared with AED 15,228 million in 2015.

Net interest income for the year declined 1% to AED 10,111 million as loan growth was more than offset by a contraction in margins.

Non-interest income declined 7% in 2016 to AED 4,637 million. Core gross fee income held steady despite a one-off impact in Q4-16 from the Egyptian Pound devaluation. There was also a decline in income from property sales and investments.

Costs for the year ended 31 December 2016 amounted to AED 4,888 million, an increase of 4% over the previous year on the back of late 2015 growth in anticipation of increased business volumes, which has since been contained in light of the new economic reality. The cost to income ratio rose by 2.1% y-o-y to 33.1%. Excluding one-offs, the cost to income ratio is 33.2%.

During 2016, the Impaired Loan Ratio improved by 0.7% to 6.4%. The impairment charge of AED 2,608 million during the year was 23% lower than in 2015 as the net cost of risk improved. This net provision includes AED 3,071 million of write-backs and recoveries, and together helped boost the coverage ratio to 120.1%.

Net profit for the Group was AED 7,239 million in 2016, 2% above that posted in 2015. The increase in net profit was driven by asset growth and higher recoveries which helped offset lower non-interest income.

Loans increased by 7% and Deposits grew by 8% during 2016. The Advances to Deposits Ratio remains comfortably within Management’s target range at 93.4%. During 2016, the Bank prudently raised AED 20.3 billion of term funding through private placements, a public sukuk issue and a club loan. Term funding now represent 12% of total liabilities, further boosting structural liquidity.

As at 31 December 2016, the Bank’s capital adequacy ratio and Tier 1 capital ratio were 21.2% and 18.7% respectively.

Business Performance

Retail Banking & Wealth Management (RBWM)

RBWM reported total income of AED 6,171 million for 2016, up 8% from 2015. Net interest income grew 7% to AED 3,783 million while fee income rose 11% to AED 2,388 million, led by growth in wealth, foreign exchange and credit card businesses. Fee income now accounts for 39% of total income compared to 30% in 2013.

Despite tighter liquidity conditions, liabilities grew by AED 28 billion or 25% during 2016, improving market share by over 2%. Low cost Current & Savings Account (CASA) balances grew by AED 9.6 billion or 10% led by salary transfer and balance enhancement campaigns.

Total advances grew 14% during 2016 to AED 38.7 billion, led by credit cards and mortgages. Our innovative Flexi Loans, launched recently to offer customers variable rate personal loans, now contributes about one-third of new business.

The business continued to focus on higher value customers with a 33% increase in sourcing affluent Priority Banking customers during 2016, and a 26% increase in emerging affluent Personal Banking Beyond customers. Over 50% of new credit cards business were in the premium segment.

RBWM continued to lead the digital banking space with the launch of Emirates NBD Pay, a contactless payment service allowing customers to make in-store purchases instantly via their mobile banking app, a first in the region. The bank opened the Branch of the Future showcasing emerging breakthroughs in banking and payment technology. The Emirates NBD Future Lab™ was set up as part of the Bank’s digital strategy to foster innovation and accelerate development of next generation digital services.

DirectRemit, the 60-second money transfer service was expanded to Sri Lanka and Egypt and continued to grow rapidly with a 60% increase in transactions during 2016. GlobalCash, a multi-currency travel card, was launched to offer customers a convenient travel and shopping experience. Dnata credit cards were relaunched, offering instant earning and redemption of loyalty points at various outlets.

Despite volatility in global capital markets, the Private Banking business witnessed an exceptional year. The unit was able to acquire additional AUMs and grow revenues from core markets and new customer segments. Furthermore, a number of bespoke and segment-specific solutions were implemented to meet the diverse needs of clients in a low-yield environment.

Wholesale Banking (WB)

Despite low credit growth and asset margin pressures due to tougher liquidity conditions, Wholesale Banking delivered a strong set of financial results for 2016 with net profit of AED 3,532 million, up 37% over the previous year, backed by continued growth in the core business, lower provisions due to improved credit quality of the loan book and strong recoveries.

Net interest income of AED 3,092 million for 2016 was 14% lower than the previous year mainly due to a re-alignment in internal transfer pricing partially off-set by higher income from a growth in lending activity coupled with a strong emphasis on margin management.

Fee income of AED 1,206 million for the year ended 31 December 2016 was 8% lower than the previous year on lower one-off investment gains and a decline in lending-based fee income due to pricing pressures. Wholesale Banking continues to focus on improving capital efficiency through growth in non-funded income especially from trade, cash management and debt capital markets activities with the sale of Treasury products in particular showing good growth in 2016.

Costs were up 21% for 2016 compared with the previous year mainly due to organizational re-alignment, an increase in Wholesale Banking’s share of the cost of Bank’s distribution network and selective initiatives undertaken to reshape the business. Wholesale Banking is investing in upgrading its Transaction Banking systems to digitise and improve levels of straight through processing and in Global Markets & Treasury where the system upgrades will support the Bank’s significant enhancement in product capabilities and digitisation initiatives.

The credit quality of the loan book continues to improve whilst the successful resolution of legacy portfolio issues led to increased recoveries. This resulted in improved provision coverage and an 83% fall in provisioning requirements to AED 340 million for the year ended 31 December 2016.

Despite relatively weak corporate loan demand in the UAE, assets grew by 5%. Deposits were lower by 6% largely reflecting efforts to optimise the cost of funding by reducing the level of high yield deposits.

Wholesale Banking continues to make good progress in its transformation programme, aiming to become the leading Wholesale Bank in the Middle East and North Africa and has recently concluded industry specific customer segmentation to have a more focused approach in providing a full range of Wholesale Banking products and solutions to the Bank’s customers across the Region.

Global Markets & Treasury (GM&T)

GM&T reported a total income of AED 380 million for 2016 a 91% growth over 2015. Income witnessed strong growth in 2016 driven by Sales and Trading desk revenue, and partly due to realignment of internal management reporting.

Key contributors to revenue growth were:

- GM&T Sales Desk revenue saw an increase of 13% due to higher volumes in Interest Rate hedging products, Foreign Exchange & Fixed Income sales.

- GM&T Trading Desk delivered a good performance on the back of strong results from Credit & FX Trading. Derivatives trading faced a challenging year as geopolitical risks in regional markets contributed to lower liquidity.

- GM&T Global Funding Desk helped raise AED 20.3 billion of term debt through AED 10.4 billion of private placements in 6 currencies, a AED 3.7 billion Sukuk issue and tap on behalf of Emirates Islamic and a AED 6.2 billion club deal

- GM&T ALM Desk undertook several initiatives to diversify the Group’s liquidity pools and successfully marketed deposit products, raising in excess of AED 20 billion at satisfactory pricing levels. The ALM Desk also played a lead role in the ongoing development of the EIBOR and LCR policies of the UAE Central Bank.

- Several system and risk management upgrades were successfully implemented in 2016 which will further improve pricing and risk controls going forward. Certain other operational advances were made including the establishment of a derivative-counterparty friendly vehicle and centrally clearing OTC derivatives through the London Clearing House.

Emirates Islamic (EI)

Emirates Islamic recorded a net profit of AED 106 million in 2016, amidst challenging market conditions. EI reported growth of 3% in total income (net of customers’ share of profit and distribution to Sukuk holders) amounting to AED 2.5 Billion compared to AED 2.4 Billion in 2015. Financing and Investing Receivables grew by 6% to AED 36 billion and Customer Deposits grew by 5% to AED 41 billion. EI’s focused approach to improve its liabilities mix led to a significant increase in CASA balances. As at end of 2016, CASA represented 67% of total customer deposits. EI’s Headline Financing to Deposit ratio at 88% remained comfortably within the management’s target range.

EI successfully issued a US$ 750 million 5-year Sukuk under its USD 2.5 billion certified Issuance programme, followed by a USD 250 million tap of the same issue. The issue, rated A+ by Fitch and listed on NASDAQ Dubai and the Irish Stock Exchange, received overwhelming investor interest across the globe and marked EI’s successful return to the international debt capital markets after a period of four years.

In December 2016, EI successfully completed an AED 1.5 billion rights issue which further strengthened its capital base.

During 2016, Fitch affirmed EI’s long term Issuer Default Rating of ‘A+’ with a Stable Outlook.

Outlook

Emirates NBD expects UAE economic growth at 3.0% in 2016, down from 3.8% in 2015, as lower oil prices are expected to have contributed to a tighter fiscal policy and slower growth in the non-oil sector. We expect the UAE’s growth to recover to 3.4% in 2017, with Dubai expected to enjoy stronger growth on the back of increased investment in infrastructure ahead of Expo2020. Higher interest rates and a strong dollar will continue to pose headwinds to non-oil growth, particularly in the Services sectors. Cuts to oil output in line with the OPEC agreement could further weigh on growth in Abu Dhabi. The Bank will continue to implement its successful strategy built around five pillars which include delivering excellent customer experience with a digital focus, building a high performance organisation, driving core businesses, running an efficient organisation and driving geographic expansion.

UAE

UAE