A record quarter for retail lending, deposit growth & customer transactions

A record quarter for retail lending, deposit growth & customer transactions

Dubai, 21 April 2022

Emirates NBD delivered its highest quarterly profit since 2019. Profits jumped 18% to AED 2.7 billion as Q1-22 was a record quarter for retail lending, deposit growth and customer transactions. Credit quality across the Group's footprint continues to improve with impairment down 20%. These results build on the economic recovery momentum from 2021. With its strong profitability and balance sheet it is extremely well positioned for expected rising interest rates and will continue to invest in its international and digital capabilities to support further growth. Emirates NBD is proud to have played a leading role in the DEWA IPO, delivering customers a fully digital platform from on-boarding and subscription through to payment.

Key Highlights – First Quarter 2022

- Increase in operating performance as loan and deposit mix improved on continued record demand for retail financing, an efficient funding base and a substantially lower cost of risk

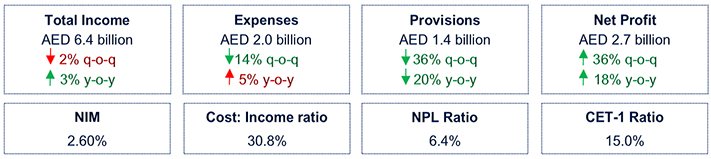

- Total income up 3% y-o-y to AED 6.4 billion on improved loan mix and cheaper deposits with initial signs of higher rates starting to feed through to margins

- Net interest margin guidance raised by 15bps in light of expected higher interest rates

- CASA grew by a record AED 18 billion, further improving funding costs

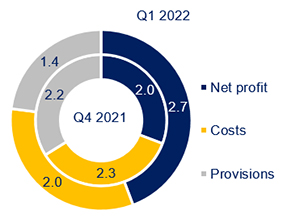

- Expenses well controlled, increasing 5% y-o-y with higher staff costs driving an increase in underlying earnings and investment in future growth particularly in our international network and digital capabilities

- Impairment allowances down substantially 20% y-o-y reflecting improving operating environment

- Resulting net profit of AED 2.7 billion, up by a healthy 18% y-o-y and 36% q-o-q

- Emirates NBD's strength empowers its customers to benefit from a growing economy

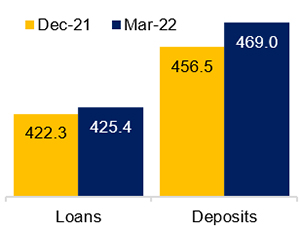

- Total assets: up 1% at AED 694 billion despite the Turkish Lira depreciation

- Customer loans: up 1% at AED 425 billion with Q1-22 another record quarter for retail financing

- Deposit mix: highest ever CASA balance, increasing by AED 18 billion in Q1-22, positioning the Group very well for rising interest rates

- Credit quality: NPL ratio increased marginally by 0.02% to 6.4% during Q1-22 with coverage ratio strengthening to 128.5% reflecting the Group's prudent approach to credit provisioning

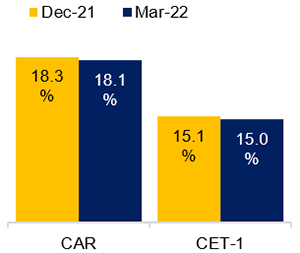

- Capital and Liquidity: 157.4% Liquidity Coverage Ratio and 15.0% Common Equity Tier-1 ratio reflect the Group's solid balance sheet, used to empower customers and create opportunities to prosper

- The Group is proactively meeting the changing needs of customers through digital innovation by offering best-in-class customer service and products while further expanding its international presence

- IPO: leading role in the DEWA IPO, delivering customers a fully digital platform enabling a seamless, paperless journey from on-boarding and subscription through to payment

- Advanced Analytics: four exciting ‘Use Cases' well underway to identify untapped customer service and revenue streams by scrutinising 21 million daily customer data points

- International: international revenue diversifies income, representing 37% of total revenue

- ESG report: published in February detailing many exciting achievements

- Environmental: decreased our environmental impact

- 6% reduction in total Greenhouse Gas emissions

- 12% reduction in energy consumption with cost savings of AED 3.7 million

- 22% reduction in water consumption

- 40% of new cards are biodegradable

- Supporting Mastercard Priceless Planet Coalition to restore 100 million trees by 2025

- Social responsibility:

- Two thirds of branches now disability friendly

- Women in senior management positions increased to 15% and we committed to grow this to 25% by 2027

- Governance:

- Welcomed three new Directors including first female Board member appointed by Shareholders

Hesham Abdulla Al Qassim, Vice Chairman and Managing Director said:

- “Emirates NBD’s profits jumped 18% y-o-y to AED 2.7 billion, reflecting the strengthening regional economy and the success of the Group’s diversified business model.

- Emirates NBD is proud of its leading role in the DEWA IPO, delivering customers a fully digital platform from on-boarding and subscription through to payment

- As a Premier Partner and the Official Banking Partner for Expo 2020 Dubai, Emirates NBD has successfully affirmed its position as a regional leader in global banking innovation by demonstrating its vision for the future of banking to the world.

- We published our Annual ESG Report, detailing many exciting ESG achievements in 2021 and further increased our target for women in senior management over the next five years.

- In February, shareholders elected three new Directors to the Board, including Her Excellency Huda Syed Naim AlHashimi.”

Shayne Nelson, Group Chief Executive Officer said:

- “Emirates NBD delivered strong results with income growth and lower provisions driving profitability 18% higher y-o-y.

- We delivered loan growth in the first quarter of 2022 reflecting the more optimistic economic outlook.

- We have increased margin guidance in light of rising interest rates.

- International operations contributed 37% of total income in Q1-22 and DenizBank’s profitability was stable despite the depreciation in Turkish Lira.

- These strong results, along with the positive outlook for margins, enable us to invest in our international network and digital capabilities, supporting our next stage of growth.”

Patrick Sullivan, Group Chief Financial Officer said:

- “We have maintained good income growth momentum, kept a firm control of costs and seen a consistent decline in the cost of risk.

- Net interest income grew by 4% y-o-y on an improved loan and deposit mix. CASA grew by a record AED 18 billion in the first quarter and the improved funding mix positions us very well for rising interest rates expected throughout 2022.

- Non-funded income also grew, helped by an increase in transaction volumes and growth in customer foreign exchange and derivative business.

- The expected increase in interest rates has enabled us to raise our NIM guidance and refine our Cost to Income ratio guidance.

- The diversified balance sheet, solid capital base and strong operating profitability are core strengths of the Group.”

Financial Review

Operating Performance

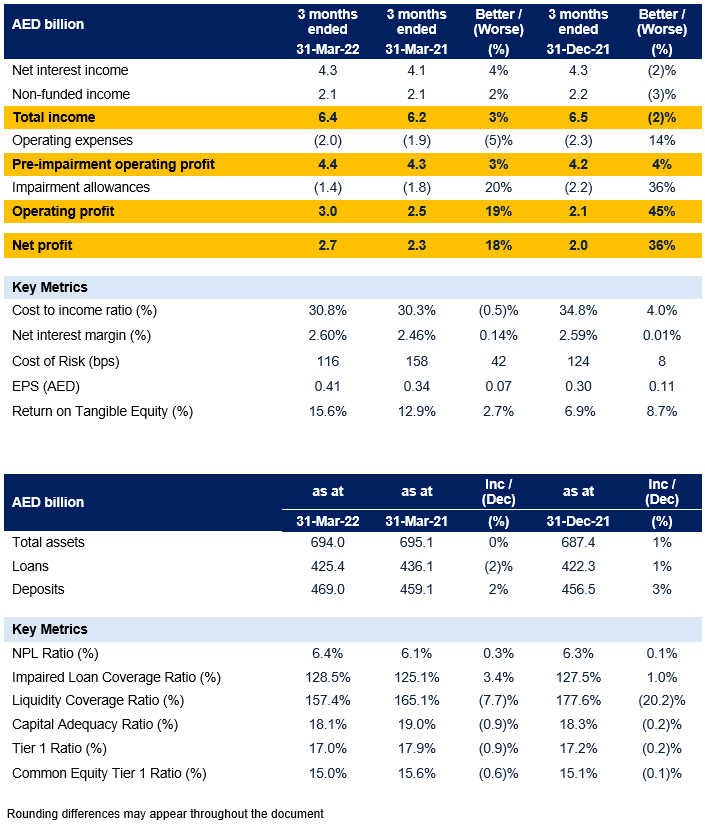

Total income for Q1-22 was up 3% y-o-y to AED 6.4 billion. Net interest income was up 4% y-o-y on improved loan and deposit mix with initial signs of higher rates feeding through to margins. Record CASA balances improved funding costs and the balance sheet is well positioned to benefit from rate rises. Non-funded income was up 2% y-o-y from increased local and international card transactions, coupled with growth in FX & Derivative income.

Expenses remain well controlled and within guidance. Higher income from anticipated rate rises enables refinement of Cost to Income ratio back to longer term target of 'within 33%'. Staff costs increased y-o-y driving an increase in underlying earnings and future growth. Other costs were lower due to seasonality from earlier campaigns.

Impairment allowances in Q1-22 were down substantially 20% y-o-y reflecting the improving operating environment, with 116 bps cost of risk within guidance.

The Group's net profit of AED 2.7 billion for the first quarter is 18% higher y-o-y and 36% higher q-o-q.

Balance Sheet Trends

Loan increased by 1% in Q1-22, with another strong quarter for EI and Retail financing which grew by 6% and 4% respectively with DenizBank's net loans up 11%.

Deposit mix improved in Q1-22 with AED 18 billion growth in CASA representing a record for CASA growth.

Liquidity remains strong with the Liquidity Coverage Ratio at 157.4% and the Advances to Deposits Ratio at 90.7%.

During the quarter, the Non-Performing Loan ratio increased by 0.02% to 6.4% whilst the Coverage ratio strengthened to 128.5%, demonstrating the Group's continued prudent approach towards credit risk management.

As at 31 March 2022, the Group's Common Equity Tier 1 ratio is 15.0%, Tier 1 ratio is 17.0% and Capital Adequacy ratio is 18.1%.

Business Performance

- Retail Banking and Wealth Management (RBWM) maintained strong business momentum, delivering a record quarter for cards acquisitions, fee income and balance sheet growth

- Customer advances increased by AED 2.4 billion, whilst CASA grew by a record AED 9.3 billion in Q1-22

- Income up 11% q-o-q with RBWM delivering its highest ever income for a single quarter

- 25% market share of UAE debit and credit card spends

- Introduced the Emirates NBD Etihad Guest Credit Cards which offers some of the highest Etihad Guest earning and rewards opportunities in the market

- Launched DEWA IPO portal on Emirates NBD website with real time direct integration with DFM

- Corporate and Institutional Banking (C&IB) developing strategic partnership with major Government entities and Corporates by digitizing service platforms and leading landmark ESG transactions

- Took lead in supporting IPOs, with end-to-end IPO subscription website offering real-time on-boarding through a state-of-the-art fully digital platform

- Implemented cutting-edge new platform for businessONLINE

- Profitability boosted by higher fee income and lower impairment allowances

- Grew CASA balances, enabling the Group to retire more expensive time deposits

- Global Markets and Treasury (GM&T) delivered a strong performance with net interest income growing 171% y-o-y in Q1-22 due to higher income from balance sheet hedges and an increase in banking book investment income.

Non funded income up 31% y-o-y: - Trading desk had a successful quarter, with notable success in Rates, Credit and FX trading

- Sales and Structuring helped customers lock in favorable borrowing costs and FX rates

- Emirates Islamic's net profit up 62% y-o-y to AED 342 million on higher income and lower impairment allowances

- DenizBank net profit of AED 629 million is stable y-o-y despite 48% depreciation in currency translation

Outlook

While higher oil and food prices pose upside risks to inflation globally, higher oil prices will generate budget surpluses with the GCC economies. Emirates NBD Research revised 2022 GDP growth forecasts upwards for the GCC, factoring in expected higher oil and gas production.

Emirates NBD Research expects UAE real GDP to grow by 5.7% in 2022, up from 3.8% in 2021, helped by an increase in oil production. The Kingdom of Saudi Arabia’s economy is expected to grow 7.7% in 2022 from 3.2% in 2021 also boosted by higher oil production.

Egypt and Turkey are expected to face increased current account deficits in 2022 as food and energy import costs rise, inflationary pressures continue and earnings from tourism may be impacted by the conflict in Ukraine.

UAE

UAE